Mapping Digital Cash Flows: PCI Compliance Strategies in API-Enabled Systems for Seamless Mobile and Recurring Credit Card Transactions

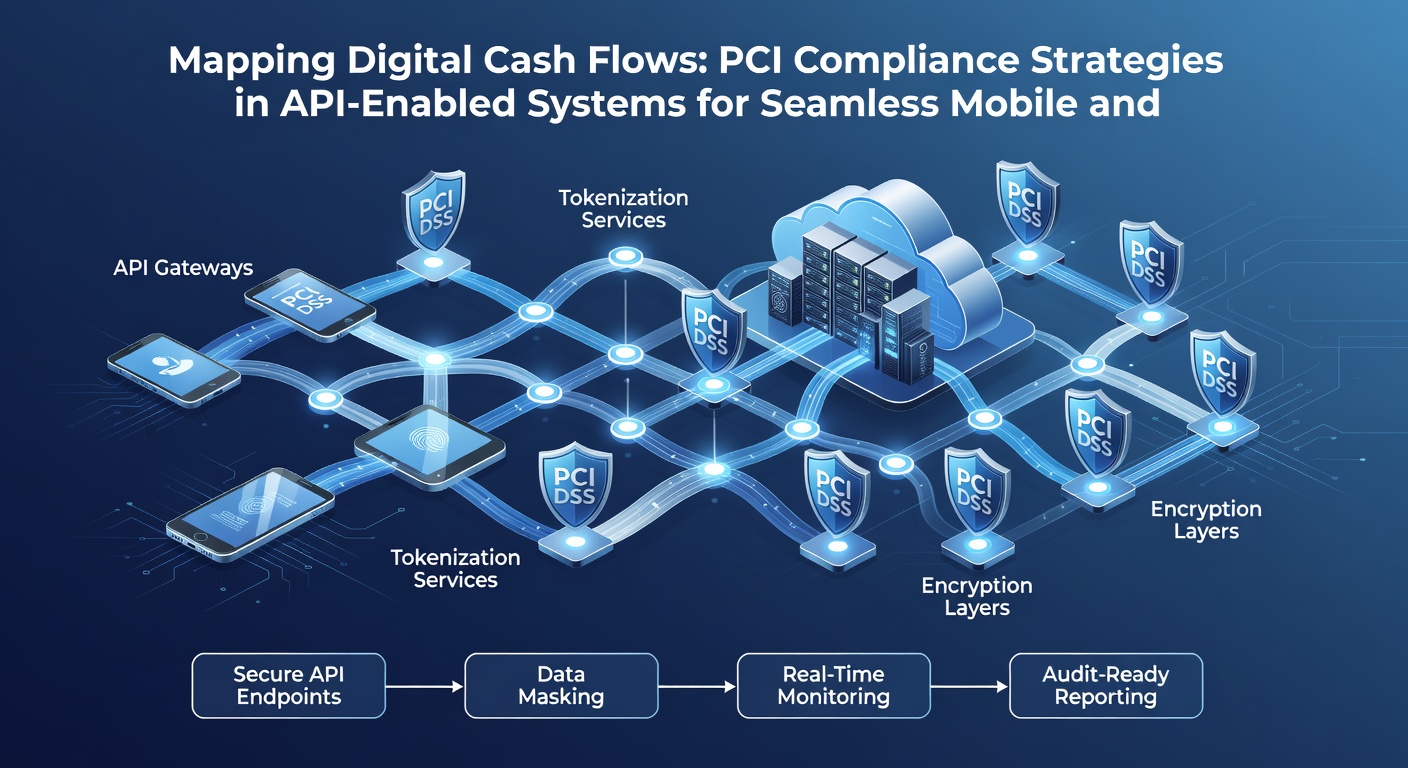

Payment networks that rely on APIs have transformed how merchants handle credit card data across mobile apps and subscription models, yet they must align every data exchange with PCI DSS requirements to protect cardholder information during transmission and storage. Observers note that these integrations create continuous flows of sensitive details between customer devices, merchant servers, and acquirer systems, which means each endpoint needs layered controls that address encryption, access restrictions, and logging without interrupting the user experience.

Researchers have documented how tokenization serves as a core technique in these environments because it replaces primary account numbers with unique identifiers that hold no value if intercepted during mobile checkouts or recurring billing cycles. Data from industry reports shows that organizations adopting tokenization reduce the scope of their compliance assessments since fewer systems actually store or process full card numbers, and this approach supports seamless renewals by allowing APIs to reference stored tokens rather than re-entering card details each month.

Core Elements of PCI DSS in API Architectures

PCI DSS version 4.0 outlines twelve requirements that cover network security, vulnerability management, and access control, while API-specific implementations add considerations for authentication protocols and rate limiting to prevent brute-force attempts against payment endpoints. Experts have observed that developers often embed these controls directly into microservices so that every call to process a recurring charge validates the token and confirms the merchant's PCI scope before any funds move. According to guidance from the PCI Security Standards Council, organizations must maintain an inventory of all APIs that touch cardholder data and conduct regular penetration testing focused on those interfaces.

Systems built for mobile transactions face additional scrutiny because devices connect over variable networks where man-in-the-middle risks rise, which leads teams to enforce mutual TLS and certificate pinning as standard practice. Figures from payment industry analyses reveal that mobile-initiated recurring charges grew steadily through 2025, pushing merchants to map each cash flow step from app launch through authorization and settlement so auditors can trace data lineage without gaps.

Strategies for Mobile and Recurring Transaction Compliance

Teams managing recurring billing integrate webhooks that notify systems of successful or failed charges, yet each webhook must carry only tokenized references and trigger immediate logging to meet requirement 10 on audit trails. People who design these flows often separate the payment processing service from the main application so that card details never enter the merchant's primary database, which shrinks the compliance boundary and simplifies quarterly scans. What's interesting is how this separation also speeds up feature releases because updates to the billing logic do not require revalidating the entire PCI environment.

Validation of card details at the point of initial signup still demands strong customer authentication, and many platforms now embed device fingerprinting alongside API calls to detect anomalies before the first charge processes. Studies from payment research groups indicate that combining device data with behavioral signals cuts fraud rates on recurring mobile subscriptions without adding friction that might cause customers to abandon sign-up. As May 2026 approaches, several frameworks are preparing incremental updates that emphasize continuous monitoring of API traffic patterns, which will require merchants to expand their real-time alerting capabilities around unusual transaction volumes or geographic shifts.

Mapping Data Flows and Maintaining Scope

Accurate mapping starts with documenting every API call that carries cardholder data or references tokens, including third-party services that handle retries or dunning sequences for failed recurring payments. Observers point out that failing to include these external services in the diagram can leave blind spots where data moves outside monitored channels. Organizations that automate this mapping through code analysis tools generate living diagrams that update whenever developers add new endpoints, which keeps compliance evidence current between formal audits.

Regular scope reviews become essential when mobile apps receive frequent updates because even minor changes to how an API authenticates requests can alter whether certain servers fall inside or outside the cardholder data environment. Evidence suggests that merchants who schedule these reviews quarterly rather than annually catch scope creep earlier and avoid costly remediation during annual assessments. One study revealed that companies maintaining detailed flow diagrams completed their PCI reports on time 40 percent more often than those relying on static documentation.

Conclusion

Effective PCI compliance in API-driven systems ultimately rests on continuous visibility into how card data moves through mobile and recurring channels, combined with technical controls that protect each step without slowing legitimate transactions. Organizations that treat compliance as an integrated part of their development lifecycle rather than a separate checklist achieve smoother audits and fewer disruptions to revenue streams. As payment ecosystems evolve, the same principles of tokenization, scoped APIs, and documented flows remain central to keeping digital cash movements both seamless and secure.