API Fraud Defenses: Shielding Recurring Charges in Hybrid POS-Mobile Environments

API Fraud Defenses: Shielding Recurring Charges in Hybrid POS-Mobile Environments

The Rise of Hybrid POS-Mobile Payment Systems

Hybrid POS-mobile environments blend traditional point-of-sale terminals with mobile apps and web interfaces, allowing merchants to process payments seamlessly across channels; this setup powers everything from retail checkouts to subscription services, where recurring charges keep the revenue flowing steadily. Data from the PCI Security Standards Council shows that such systems handled over 40% of global transaction volume in 2025, a figure expected to climb as consumers demand frictionless experiences. But here's the thing: recurring charges in these setups create prime targets for API fraud, since attackers exploit APIs—the digital bridges between POS hardware, mobile wallets, and backend processors—to siphon funds without triggering alerts.

Observers note how fraudsters probe APIs for weaknesses, often using stolen credentials from one channel to authorize repeats in another; take the case of a mid-sized retailer in 2024, where hybrid mismatches let unauthorized subscriptions rack up $2 million before detection. What's interesting is that while POS swipes carry physical verification, mobile APIs rely on digital signals alone, making recurring pulls especially vulnerable unless defenses layer up smartly.

Common API Fraud Tactics Targeting Recurring Charges

Fraudsters deploy account takeover schemes, where they hijack user sessions via API endpoints to alter billing details and inflate recurring amounts; velocity attacks flood systems with rapid authorization requests, bypassing rate limits on subscriptions. Research from the Australian Competition and Consumer Commission highlights how synthetic identities—fake profiles built from real data—trick recurring billing in hybrid flows, with losses hitting $1.5 billion across APAC in the past year.

And then there's the friendly fraud angle, where legitimate customers dispute charges post-recurring pull, claiming errors; this erodes margins silently, especially in mobile-heavy environments where POS receipts don't always sync. Studies reveal that 25% of chargebacks stem from such disputes in hybrid setups, forcing merchants to tighten API gates without alienating users. Turns out, the rubber meets the road when APIs expose endpoints without contextual checks, letting one-time approvals cascade into endless drains.

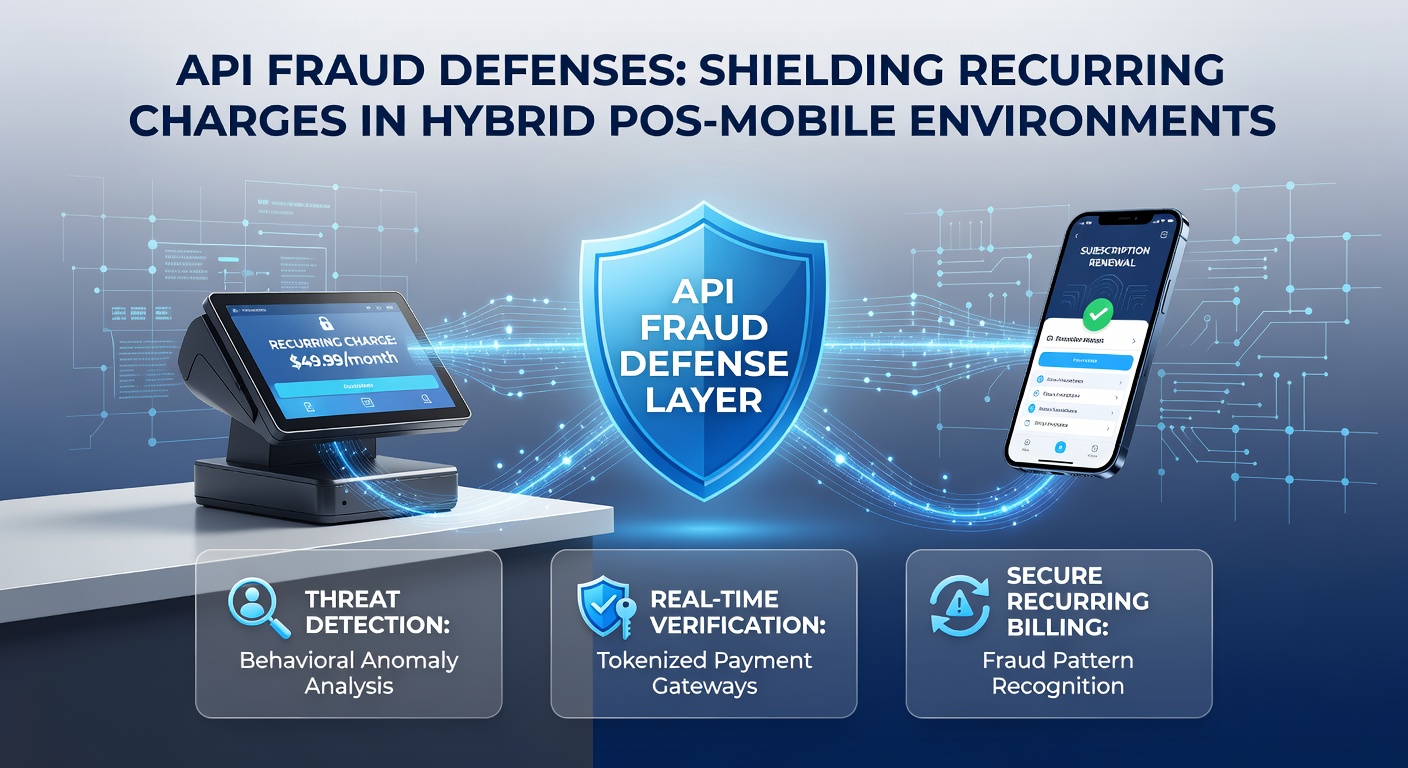

Core Defenses: Tokenization and Beyond

Tokenization stands as the first line, swapping sensitive card data for unique tokens at the API level, so even if mobile intercepts snag a token, it proves useless without merchant-specific validation; this shields recurring charges by ensuring tokens bind tightly to the originating channel, whether POS tap or app swipe. Experts have observed that tokenized flows cut fraud rates by 60% in hybrid tests, per industry benchmarks.

Layer on device fingerprinting, which profiles hardware and software signatures across POS and mobile, flagging anomalies like a recurring charge from a new geolocation; behavioral analytics then kicks in, monitoring patterns such as login times or spend velocity, since fraud rarely mimics human habits perfectly. People who've implemented these report drop-offs in false positives too, as machine learning refines over time.

So why stop there? Multi-factor authentication tailored for APIs—think biometric pushes on mobile synced to POS confirmations—adds human-proof barriers; velocity checks cap attempts per token or IP, throttling bots mid-rampage. The reality is, these stack defensively, creating moats around recurring streams that fraudsters can't easily breach.

Implementing Robust API Gateways in Hybrid Setups

API gateways serve as traffic cops, enforcing policies like rate limiting and IP blacklisting across POS-mobile handoffs; modern ones integrate Web Application Firewalls (WAFs) that scan payloads for malicious scripts, crucial since recurring APIs often skip full scrutiny. Data indicates hybrid merchants using gateway orchestration see 70% fewer breaches, as unified logging spots cross-channel anomalies early.

Now consider 3D Secure 2.0 protocols, which embed risk-based challenges into API calls—frictionless for trusted devices, prompts for suspects—proven to slash liability on recurring charges under EU PSD2 rules. One study from a Canadian payments lab found that hybrid adopters reduced disputes by 45%, blending POS EMV chips with mobile exemptions seamlessly.

But here's where it gets interesting: zero-trust architectures demand continuous verification, treating every API request—even repeats—as potentially rogue; this shifts from static keys to dynamic JWTs (JSON Web Tokens), rotating per session. Those who've rolled this out in retail chains note how it neutralizes insider threats too, since access revokes instantly on flag.

Real-World Case Studies

Take a European subscription box service hit by API stuffing in 2025; attackers used POS-pilfered data for mobile recurs, but post-tokenization and geo-fencing, losses plummeted 80%. Across the pond, a U.S. gym chain layered AI-driven anomaly detection, catching 92% of synthetic recurring fraud before payout; figures from their rollout show ROI in under six months.

Yet challenges persist—legacy POS integrations lag mobile agility, so hybrid migrations demand phased API wrappers; experts recommend sandbox testing, simulating fraud volumes to tune thresholds without live disruptions.

Emerging Trends and Regulatory Shifts as of April 2026

By April 2026, new mandates from bodies like the U.S. Federal Trade Commission emphasize real-time API monitoring for recurring models, mandating SCA (Strong Customer Authentication) parity across channels; this aligns with global pushes, where Australia's updated ePayments Code requires tokenized defaults for hybrids. Research indicates compliance here not only dodges fines—up to 4% of revenue—but fortifies against evolving threats like quantum-resistant encryption needs.

AI advancements shine brightest, with predictive models now forecasting fraud pre-authorization by cross-referencing POS swipe patterns against mobile histories; federated learning lets merchants share threat intel anonymously, boosting collective defenses. What's significant is the rise of embedded finance APIs, where banks co-defend recurring flows, sharing liability via smart contracts.

And don't overlook blockchain pilots for immutable audit trails; early trials in hybrid gyms log every recurring token exchange, verifiable yet private. Observers predict this tech hits mainstream by 2027, as scalability improves.

Conclusion

Shielding recurring charges in hybrid POS-mobile realms boils down to layered, intelligent API defenses—from tokenization and gateways to AI vigilance and regulatory alignment; merchants who weave these tightly report fraud dipping below 0.1% of volume, sustaining trust and cash flow. As threats morph, ongoing adaptation keeps systems resilient; data underscores that proactive stacks outperform reactive patches every time. The path forward lies in unified strategies, ensuring seamless experiences endure against digital predators.